Phew, it sure has been a long time since I’ve updated my blog! Thankfully I have a day off work today, so I decided to take advantage of the bad weather to inform you guys on my progress. First up is an overview of my net worth after the first quarter of 2016.

In the past I used to publish net worth updates every single month, but from now on I’ll stick to quarterly updates. There’s two main reasons for this change of heart.

First, my total net worth doesn’t matter all that much since I’m a dividend growth investor first and foremost. That means I try to steadily grow the passive income of my portfolio rather than the underlying capital. Of course, I could be making awesome progress with regards to dividends, but have a stinky total return due to capital loss, so it’s not as black and white – hence the quarterly updates.

Second, it’s harder being a long-term investor if you’re confronted with the perception of a wildly volatile portfolio. Indeed, the total value of my holdings varies daily, sometimes by €1,000 on any given day. And let me tell you, that’s tough psychologically. By reviewing your portfolio on a less frequent basis you take away the daily swings and thus the perception that your investments are volatile.

So let’s see what Q1 in 2016 brought us!

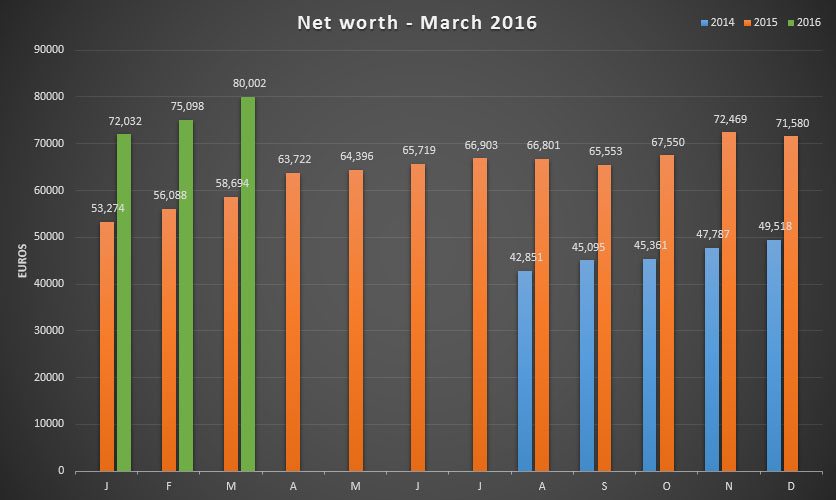

Compared to the end of 2015 my net worth grew by a staggering 7,970 Euros! Most of the increase obviously comes from my excellent savings rate, but a large chunk can be attributed to the performance of the stock market. Even though January and February were dreadful months for most indices, March picked up the pace and pushed my dividend portfolio and exchange-traded funds to new heights – perception is key, as you can see.

As a result, my overall net worth grew by 11.06% in the past three months, yay! On top of that it’s the first time ever that I, just barely, cross the 80,000 threshold. I’m slowly closing in on that illustrious six figure mark! My habit of consistently saving and investing any excess cash is paying off big time.

When you take into account that I earn about €12 an hour after taxes, that’s a massive 664 hours or 90 days of work-free capital in the bank. And that capital is now working for me, slowly building my wealth over time until I reach financial independence. Compound interest at its finest!

Dividend growth stocks

Returning visitors know that dividend growth stocks make up the bulk of my portfolio because I enjoy building a stable and passive stream of income. At the moment I’m using all dividends to fuel the compounding effect of my investments and I’ll continue to do so until I decide to retire early and live off of them.

As a result, I initiated three buys over the past couple of months, all of them in the healthcare space funnily enough. The passive income I currently receive isn’t nearly enough to initiate full positions, so of course I also add in my hard-earned and easily-saved money.

First up was Swiss-based pharma giant Novartis (VTX:NOVN), which experienced a bit of weakness in the past couple of months – and still does, for that matter. Some of Novartis’ products aren’t putting out the numbers the company expected, which weighs on the bottom-line a bit. On top of that the Swiss Frank is also hurting the pharmaceutical’s performance.

Second, I bought a larger chunck of GlaxoSmithKline (LON:GSK), the British healthcare company that recently swapped its oncology business with the aforementioned Novartis. Even though Glaxo’s numbers aren’t too rosy, they’re slowly turning around with a ton of new products in the pipeline. What pushed me to increase my stake in GSK is management’s decision to pay a special dividend this year on top of the already high yield, signalling strong belief in the company’s cash-flow rich future.

And third, I bought another beaten-down stock, namely Sanofi SA (EPA:SAN). French Sanofi mostly focusses on cardiovascular solutions, diabetes, oncology and vaccines, and is a leading player in all of these areas globally. Currently, however, earnings growth is a bit lacking, even though the company is well-placed for the future. That’s why I took advantage of its 4+% yield.

You can find the gains in absolute and relative numbers for each company in the table below. The cost basis for each position includes the price of the shares, a 0.27% stock market tax and brokerage fees.

| Ticker | Company | Shares | Cost basis | Mkt. value | Gain |

|---|---|---|---|---|---|

| ABI | AB Inbev | 22 | 2,385.18 | 2,403.50 | +0.77% |

| AFL | Aflac Inc. | 9 | 419.41 | 500.08 | +19.24% |

| T | AT&T | 80 | 2,352.46 | 2,742.42 | +16.58% |

| BLT | BHP Billiton plc | 110 | 1,908.56 | 1,086.69 | -43.06% |

| BP | BP plc | 92 | 507.24 | 406.54 | -19.85% |

| CAT | Caterpillar Inc. | 25 | 1,465.40 | 1,681.52 | +14.75% |

| DE | Deere & Company | 7 | 452.61 | 474.14 | +4.76% |

| DGE | Diageo plc | 75 | 1885.55 | 1,1,780.85 | -5.55% |

| ENG | Enagas SA | 50 | 1,258.60 | 1,321.00 | +4.96% |

| GE | General Electric | 22 | 450.70 | 617.01 | +36.90% |

| GSK | GlaxoSmithKline | 80 | 1,470.38 | 1,425.57 | -3.05% |

| HOME | Home Invest Belgium | 30 | 2,682.00 | 2,996.70 | +11.73% |

| INDV | Indivior plc | 10 | 3.89 | 20.58 | +429.14% |

| IBM | IBM Corp. | 6 | 736.76 | 795.64 | +7.99% |

| JNJ | Johnson & Johnson | 20 | 1,769.41 | 1,899.28 | +7.34% |

| KIN | Kinepolis Group | 40 | 1,399.25 | 1,525.20 | +9.00% |

| MCD | McDonald's Corp | 14 | 1,003.47 | 1,545.00 | +53.96% |

| MUV2 | Munich RE | 14 | 2,582.65 | 2,502.50 | -3.10% |

| NG | National Grid plc | 100 | 1,332.11 | 1,245.86 | -6.47% |

| NOVN | Novartis AG | 30 | 2,295.71 | 1,912.83 | -16.68% |

| PG | Procter & Gamble | 23 | 1,594.66 | 1,660.70 | +4.14% |

| QCOM | Qualcomm Inc. | 9 | 520.23 | 404.22 | -22.30% |

| RB | Reckitt Benckiser plc | 10 | 630.34 | 849.57 | +34.78% |

| ROG | Roche Holding AG | 5 | 1,233.71 | 1,082.66 | -12.24% |

| RDSB | Royal Dutch Shell | 110 | 2,956.64 | 2,394.70 | -19.01% |

| SAN | Sanofi SA | 15 | 1,077.36 | 1,062.90 | -1.34% |

| S32 | South 32 Ltd. | 48 | 20.04 | 47.13 | +135.20% |

| KO | The Coca Cola Company | 17 | 540.05 | 691.88 | +28.12% |

| FP | Total SA | 45 | 2,045.95 | 1,802.70 | -11.89% |

| ULVR | Unilever plc | 90 | 3,170.00 | 3,58.64 | +12.95% |

| VZ | Verizon Communications Inc. | 20 | 785.07 | 984.50 | +20.82% |

| VOD | Vodafone plc | 188 | 536.19 | 524.81 | -2.12% |

| Total | 43,471.56 | 43,933.35 | +1.06% |

Exchange-traded funds

I’ve said it before and I’ll say it again, the ETFs below have been doing exactly what they were designed to do. By tracking the MSCI World, emerging markets and Europe indices rigorously, these exchange-traded funds have experienced respectable growth in the past few months, especially the MSCI World ETF. If you’re a new investor looking for a long-term set-it and forget-it approach, I can’t recommend index funds enough.

| Ticker | ETF | Cost basis | Mkt. value | Gain |

|---|---|---|---|---|

| IWDA | iShares Core MSCI World | 6,217.44 | 7,054.04 | +13.46% |

| IEMA | iShares MSCI Emerging Markets | 1,214.59 | 1,203.12 | -0.09% |

| IMAE | iShares MSCI Europe | 3,561.94 | 3,586.88 | +0.70% |

| Total | 10,993.97 | 11,844.04 | +7.73% |

Other

The last part of my portfolio constist of a tax-efficient pension fund and good ol’ boring savings accounts. As I’m currently still rebuilding my emergency fund I added another €1,000, while my pension fund receives automtic payments to hit the €950 upper limit for 2016.

| Name | Cost basis | Current value | Gain |

|---|---|---|---|

| Pension fund | 2,094.99 | 2,202.68 | +5.14% and 30% tax break |

| Savings account | N/A | 18,000.00 | N/A |

| Emergency fund | N/A | 4,021.55 | N/A |

| Total | 24,224.23 |

Going forward

Living frugally, saving as much as possible, and investing those savings remains the holy trifecta of financial independence. Without putting in much effort myself, my net worth continues to make big strides forward, as this update clearly shows. It’s incredible to see how fast you can get a snowball rolling as long as you remain focussed and stick to your strategy.

After the last net worth update, where I lost a bunch of money in the stock market, it’s funny to see the numbers tick back up to previous levels and surpassing what I had projected for myself. Onward and upward!

Thank you for reading and for your support.

Ciao NMW,

Long time no see!! 🙂 Great update and really great numbers I see, best compliments to you, as usual your saving rate is incredible!

Hope to see some new posts soon!

ciao ciao

Stal

Stal,

Indeed, it’s been a long time! Have been occupied by other things, mostly work and cycling a lot lately – which you must appreciate given that the Giro is on right now! 😉

My effort to build passive income and become financially independent hasn’t change though, as you can see. Seeing my net worth and income grow remains as addictive as ever!

I’m already working on more content, which I hope to get out to you guys soon.

Cheers and all the best over there,

NMW

Glad to see that thing are good, will wait for the updates! I see your PF hasn’t changed a LOT, or some trades are missing? ciao cia

Stal

Stal,

During the first quarter I only performed three trades (GSK, SAN, NOVN) on top of the ones already reported (T, ULVR). For April and May I already bought into QCOM and NG, but you’ll find these buys in the Q2 report.

Cheers,

NMW

Thanks for this article. You have confirmed my ETF choices for long term growth 🙂

Cheers

MrRicket

MrRicket,

ETFs remains a great tool for long-term asset growth indeed. And the best part is that they’re really easy to set up and require hardly any looking-after.

Funnily enough though, they’ve underperformed my dividend portfolio for the past 14 months and it seems they’re way more volatile. That’s probably down to random variance, but it’s interesting to see nonetheless.

Cheers,

NMW

I was thinking the same when I looked at the portfolio… It seems overall the ETFs still perform better (+7.7% vs +1.1%)? I can understand the allure of stock picking though – recently I bought a bit of HSBC as I could not resist the tax free 8% yield. Was it a wise choice? Only time will tell 🙂

PS Glad you are back!

Singvestor,

The ETFs are actually underperforming my dividend growth portfolio for the past year. The only reason they appear to perform better is because I bought them before the ECB introduced QE, whereas the dividend portfolio started later (and continues to be build until today). On top of that, the 1.1% of the dividend portfolio isn’t the total return since you should take the dividend income into account as well.

For the past year, the MSCI World ETF has underperformed my dividend stocks by as much as 6%, the Europe one by 14%, and the EM one by 20%. On top of that I’ve noticed that the ETFs are way more volatile than my dividend stocks. I guess that’s the advantage of stable blue chips!

Of course, the numbers above come from a very limited time span and sample set. I guess we’ll have to find out in the long-run.

Cheers,

NMW

PS: glad to be back, thanks!

Great analysis, thanks for sharing! Will be interesting to see how it turns out, but should be good since the portfolio is nicely diversified and includes only very solid companies.

Welcome back NMW. I keep meaning to take a look at GSK but they never seem to come up on my screen.

Cheers,

DFG

DFG,

Thanks, buddy! Appreciate the warm welcome back.

GSK remains one of the highest yielding quality healthcare plays out there. For 2015 they didn’t cover the dividend, but with the current earnings growth it seems like they’re well on their way to cover the dividend from 2016 onwards. Well worth a look if you can stomache a bit more risk than the standard JNJ play!

Cheers,

NMW

Nice progress NMW! A couple of months ago I also focused on expanding my healthcare exposure, I bought GSK, Sanofi and Novo Nordisk. Novartis is still on my wish list, I think I lacked the funds to initiate a position when they traded around a 4% yield some time ago.

DAC,

Great to see we’re buying into the same companies! GSK and Sanofi are incredible value right now, even with the higher short-term risks. I’ll probably double my position in Sanofi if it remains this low for the coming months.

Novo Nordisk is also on my list, but the current yield simply is too low to iniatiate a position. There’s so many other good deals out there! Besides, what’s the foreign withholding tax on Danish stocks anyway?

I hope you can add Novartis to your portfolio soon! It seems like the stock will remain near its 52w low for the coming months.

Cheers,

NMW

Novo Nordisk’s starting yield is low but I think they’ll continue to offer a high dividend growth rate given their good growth prospects. Unfortunately, Danish foreign withholding tax is 27%.

DaC

DAC,

Ouch, that takes the current gross yield of 1.7% right down to about 0.85% net. I’ll have to do some number crunching in Excel to see if it’s worth the growth prospects.

Thanks for letting me know,

NMW

Current net yield is around 0.95 percent, it’s one of the lowest yielding stocks in my portfolio but I bought it more for future rather than immediate income.

I wrote an article about them some time ago, diabetes is still a huge growth market as the number of diabetics is growing rapidly and many people with the condition are undiagnosed or not receiving proper treatment.

Outside the business as usual scenario, the pipeline contains exciting stuff like the world’s first tablet-based alternative to injection-based treatment for diabetics and they’re also applying what they’ve learned in the diabetes field to tackle obesity. The latter is a largely untapped market, it’s still in the early stages and there are a lot of hurdles to clear but if Novo Nordisk can get this ball rolling it could be huge.

Looking good! If you continue that pace, you should rush by the magical 100.000 € within this year easily. It also took me approximately 3 years to reach that mark. However, I have stepped up the pace in the middle of 2015, where i started to develop and follow my own strategy.

Always good to see some fellow Europeans embarking on a similar project!

Stay the course!

Finanzr

Finanzr,

The six figure mark will be a stretch, but I’ll sure try to get there. With a bit of luck from Mr. Market and some extra frugal efforts, I should sail right by!

Three years is an incredibly short time to reach €100.000 though, congrats! I already had about 30-40.000 euros in savings when I started my FI journey, so it took me quite a while longer to get there… Let’s say 27 years! 🙂

Best of luck to your own effort,

NMW

Nice progress NMW. Good to know that you’re still busy with increasing your net worth and getting paid dividend income for doing nothing at all.

Thanks, Tawcan! Doing our best, one day at a time!

As a fellow Belgian, I’m always excited to see a new post appear. Gratz on the progress!

I’m hoping you’ll find the time to answer some of my (lengthy) questions:

– I recently just started out on my investing journey by buying a small (30) amount of $AAPL stocks as I believe they’re a great company. They have a balance sheet most companies would kill for, own mountains of cash, have a P/E of about 10,and generate an absurd amount of revenue. They’re definitely experiencing some growth issues as the smartphone market seems to be pretty saturated, but I’m a strong believer. My question: what’s next? Do I slowly expand my portfolio “company by company”, or am I better off investing in multiple companies all at once, and slowly increase my position? And a related question: as a rookie, how did you determine the size of your position?

– How do you feel about having some overlap in your portfolio? As you own 3 pretty diversified ETF’s, you automatically seem to have some “duplicate” stocks in your portfolio. Meaning you not only own shares of company X through being a shareholder, but also indirectly own a second chunk of company X via the ETF you own.

– I fully understand that having geographical diversification is a good thing, but I just don’t see the need to have an ETF right now which focuses on emerging markets as they’ve been doing horribly lately. In general, would you advise me to have a couple of ETF’s, no matter what? I originally planned on starting out with ETF’s, but realized they might not really suit me as they’re not exactly hands on. I like doing research, checking stock prices daily, etc. Doesn’t mean I like risk, but ETF’s are obviously pretty passive compared to “stock picking”. Should I have them in my portfolio anyway?

– Any tips & tricks, lessons learned, do’s and dont’s, you’d like to share with people who are just starting out, now that you can look back on your own journey of about 2 years? The thing I find myself struggling with the most is allocating my capital… How much do I put in stocks, what percentage do I keep in cash, etc….

Thanks in advance! 🙂

Investing is full of personal choices to make, directed by your situation. There are some general rules to follow. Here is what you ofte read as the best set of rules to follow

1- make sure you have diversified portfolio of investments. If one goes down, you do not loos too much. It comes down to defy ing the max position and loss you are willing to accept

2- ETFs are a great way to get this diversification, even if it creates the “overlap” between the ETF holdings and DGI stock. This is an approach you see often.

3- ETFs can be boring to deal with. Once the asset allocation is set, you execute the buy that set the portfolio towards your target allocation. Boring as hell…! and that is good. People tend to take some playmoney next to that.

In either case, you need to do your research on risk you think is best for you, the cash you think you need (many rule of thumbs available as well)

Good pointers, ATL! Thanks!

Ciamician,

Thanks for stopping by and taking the time to leave a very lengthy comment! I’m always happy to meet new people who are eager to learn.

Ambertreeleaves gave you some good pointers already, but here are a couple more:

(1) With regards to building your portfolio from scratch: it’s very difficult to start out with a diversified selection of stocks if you lack the necessary funds. I had a bit of cash on hand, but not too much, so I ended up with a middle-of-the-road approach through free transactions costs for three months. If I were in your shoes, however, I’d slowly go from company to company. I think you’d do well to create a wishlist and buy any opportunities that present themselves. When you reach about 15-20 stocks you can start diversifying actively, picking stocks or sectors over other for the sake of diversification.

Buying into a bunch of companies at once will probably recude your initial position in them to the point that brokerage fees are going to eat you alive, so I would advise against that. Brokerage fees were also a good starting point to determine the initial size of my positions: I tried keeping the costs between 1-1.5% of every transaction. In the long-run I’m trying to limit every stock position to a size of max 5% of my total net worth.

(2) Overlap doesn’t bother me too much. I know that most of my individual stocks are also in the ETFs or the pension fund I own, but only make up a very small fraction of them. It’s no big deal.

(3) Always remember that past performance is no indiciation of future performance! 😉 I know that EM aren’t doing too well at the moment, but we’re playing a long-term game here. Of course, having EM in your portfolio is a personal choice and if you’d rather stick to the more mature Western markets, who am I to say that’s wrong? There’s merit in both choices.

ETFs were a perfect way for me to learn how the stock market worked, to deal with the volatilityof the market, and as a way to quickly diversify my base portfolio. That’s why I often recommend them to new investors, but it’s no golden rule of course. If you like a more active approach (be sure not to turn into a trader, ha!) then you can ignore them altogether. Again, it’s a personal choice here and I can’t make it for you.

(4) The only tips that apply to everyone are: save as much as possible and invest as much as you’re comfortable with. The stock/cash/bond allocation of your portfolio is something you’ll have to figure out yourself, but some basic questions you could ask yourself: how much do I need to have in emergency money? (e.g. six months of income set aside); am I looking to buy a home in the near future? (increase cash if you do); what’s my age? (stock/bond allocation); can i stomache losing x% of my money? (increase/decrease exposure to stocks), etc.

As you can see I have a pretty large cash cushion(25%), especially for someone who is very jobsecure. Having that cushion gives me piece of mind and offers flexibility when it might be needed. My other savings are all invested in the stock market.

I hope this was helpful – let me know if you have any further questions.

Cheers,

NMW

Thanks for taking the time to answer my questions, really appreciate it 🙂

Funds aren’t exactly the problem, I’m circling around your net worth just to give you an idea. I’m 25, so I’d say we’re in a pretty similar position. I’m still trying to learn as much as possible and trying to refine my strategy when it comes to picking a certain stock… which is now limited to looking for blue chip companies with a reasonable P/E (~ 10) and are near their 52wk low. Perhaps not the best strategy. Right now I’m looking at EBR:AGS, AMS:INGA and ETR:BMW.

I’m using Binck, which means I have 1100 EUR of “free” brokerage costs till the end of June, as I’m a new customer. So now would the ideal time to stock up on stocks (pun intended) 🙂 Would you advise the dollar cost averaging or the all-in approach when it comes to stocks?

And a final question: any particular reason why your % of ETF’s is quite modest and seem to have little activity (in terms of increasing your position) compared to your stocks?

Ciamician,

You’re two years ahead of me then! 😉

If I were you I’d build a whole bunch of smaller positions until the end of June. Maybe not go all-in, but 50/50? I can’t really advise you on that, but I think you’ll have a good feeling for yourself if you’re ready to start investing.

As to why my ETFs are relatively small: I started out with ETFs as a way to learn about the stock market and to quickly diversify my portfolio. Now I just keep them around as I focus on DGI 100%!

Cheers,

NMW

To start investing in stocks (almost) from scratch, how fast would you go in? A certain percentage of net worth a month?

Got my first Solvay dividend the other day, pretty cool 🙂

Schlong,

There’s two schools of thought: dollar cost averaging and all-in.

The advantage of averaging a certain percentage of your net worth every month insures that you don’t buy at the top of the market, but rather have an average entry position. For ETFs I would definitely take this approach.

The all-in approach basically tells you to dump your cash into the market as fast as possible. Some studies have shown this strategy to be the most effective in the (very) long-run, with only very minor exceptions. If you’re purchasing individual stocks this might be a good option if you see enough opportunities in the market.

Congrats on the Solvay dividend! Another dividend stalwart I would like to add to my own portfolio in the future. 🙂

Cheers,

NMW

Good to see you are still looking at finances.

Great results.

Recently, i added solvay as second official dgi stock to my portfolio. The dividend was great to get!

Amber tree

ATL,

Congrats on the Solvay dividend! Seems like you and Schlong had the same idea. Some time in the future I would like to own Solvay too.

Best of luck with any future DGI purchases!

Cheers,

NMW

After some research, solvac would be even better.

Thanks for letting me know, ATL! I didn’t know that so I’ll definitely look into both Solvay and Solvac.

Let us know your idea… I consider switching

Hi NMW

I have tried buying shares of Solvac but its very hard for individual persons. I have done a lot of research about it and apparently you cant do it yourselves but need the help of a banker or something because the shares are on your own name and personalized.

I figured it wasnt worth the effort and mess although I bought for more than €6000 Solvay shares. I’d say if you go really high in cash okay, but it will seriously cost some time and effort.

WDYR,

Thanks for the input! I’ll make sure to look into Solvay and Solvac properly. If it’s as difficult as you say, I’d rather own the Solvay shares since they’re easily traded on the Brussels stock exchange.

You’ve got quite a large position in Solvay, wow. Impressive dividend income too!

Cheers,

NMW

Wow, 80.000€, great to see your progress! You´re working hard to get the 100.000€, i think it´ll be an awesome moment for you, when you get it soon.

But sure, the bookvalue is not the best thing, the dividends, coming from that portfolio are much greater. I´m excited to see your next Dividend Income update soon. May was a great dividend month for me, beacause of the german dividend payers (pay 1 time a year). This month i nearly got the same amount of dividend income as the full last year!! Awesome! It´s so much fun to see the dividend income growing and knowing, that`s just the early beginning!

DividendKiddy

DK,

Thanks, buddy! Nice and smooth progress towards the first 100,000 – just how we like it!

You’re absolutely right that the value of my portfolio isn’t all too important. It’s in the dividends, of course! And for us European investors the dividend season is a welcome gift throughout April, May and June. My numbers are way up too.

Pretty amazing that you managed to make as much dividends in just one month as the entire past year! Keep it up and you’ll be amazed where you end up in a couple of years.

Best of luck,

NMW

Love your blog, keep it up, you’re doing great. I was roughly at the same level as you when I was at that age. It took me just over the first 10years of my adult life to get to my first 100k. Wasn’t much in the investment game at that time, more dreaming of it,only risking the odd 1k here and there, most came from serious saving through fear that being on a low wage for the rest of my life and not being able to retire till very old.

My next 100k came over the next 6yrs, delayed a couple of years by the 2008 crisis. Since then I’ve changed my strategy from buying traditional dividend paying shares to going for once popular now unloved shares that were on a long dividend hiatus, sacrificing investment growth on new buys during this period. It’s a high risk strategy and my fingers were burn’t at the start of this part of my journey but 6-7years later dividends have started coming through for this part of my portfolio which are showing great protential for the future.

I was expecting that reaching my future net worth goal would come first then move me onto a goal of a consistent FIRE supporting income but looking as it is now I may end up acheiving my FIRE income goal first due to potential of dividends ramping up quicker which then supports getting to my net worth goal quicker. If my future dividend strategy continues to follow the analysts predicted increase rates over the next two years then it’ll position me to reinvest the new income stream into getting balanced portfolio of dividend payers and a safety net in place.

Reckless Saving,

Inspirational story, thanks for sharing! People always say the first €100,000 is the hardest and you seem to validate that statement: 10 years for the first 100k, 6 years for the next.

At the moment I’m focussed on dividend income rather than dividend growth. That way I hope to get my portfolio off the ground quick through re-investment. As time goes on I’ll definitely shift towards low income, high dividend growth stocks. It’s amazing to see what double digit dividend growth does to your income levels over a number of years.

Best of luck getting to your FIRE income level!

Cheers,

NMW

NMW is back with vengeance! Nice progress from the financial muscles from Brussels. Seems you have been keeping yourself financially healthy with the new purchases. Keep it up.

Ha, I read vengeance in the voice of Scorpion from Mortal Kombat: “Vengeance will be mine!” https://www.youtube.com/watch?v=HMb5EhEkuOA

Thanks, buddy! I appreciate the (way too) kind words. Hope everything is great on your end too.

Cheers,

NMW

Hi NMW,

good to have you back. Keep it up!

Congratulations to your progress.

Best wishes from another European investor.

rickrack

Thank you, Rickrack!

Glad to be back.

I’m always happy to see other European investors pop up – we’re underrepresented in the financial independence and dividend growth investing scene.

Best wishes,

NMW

Well done NMW – excellent results! You are clearly rapidly approaching an important milestone, the 6 figure mark. It pays to be frugal 🙂

Mrs. SF,

Ha, the six figure mark – so looking forward to breaching it! I’ve heard it’s by far the hardest, so I can only imagine how fast I’ll get the snowball rolling towards €200k.

Thank you for taking the time to stop by and leave a comment. I’ll keep an eye on your entrepreneurship series!

Cheers,

NMW