“Well, this is going to be interesting” was the first thought that popped into my head when I sat down to write this article. As you all know, the equities markets have been off to one of the worst starts to the year ever in 2016, so that doesn’t bode too well for the little financial independence portflio I’m trying to put together. And boy, how right I was!

When I published my 2015 goals report, I thought a big spike upwards in net worth was on the table for January, but the markets decided otherwise. However, I’m still incredibly satisfied with the massive growth my portfolio underwent last year. Proud too, because large parts of the increase came from sticking to my rigorous savings regime since my investments trailed flat for the entire year.

2016 isn’t off to the best of starts though, as you can read about in detail below. When everyone woke up from their New Year’s Eve buzz the markets decided to reward us with a financial hangover that has many investors frightened judging by the amount of e-mails I’ve received. Even Royal Bank of Scotland believes we’re in for a “cataclysmic” year, whoa!

Hide yo kids, hide yo wife!

But here’s the catch. A dividend growth investor doesn’t really care about his net worth all too much. He or she doesn’t plan to touch the principle of his or her investments anyway. The income and interest those investments throw off are the real prize money, so that’s what dividend growth investors focus on.

Besides, it’s a lot easier to not let your emotions get the better of you when you focus on the stable dividend income from the quality companies you own instead of the volatile day-to-day value of their stock price. Even with the relatively large downturn in the market, my passive income remains the same. And that’s why I love dividend growth investing so much.

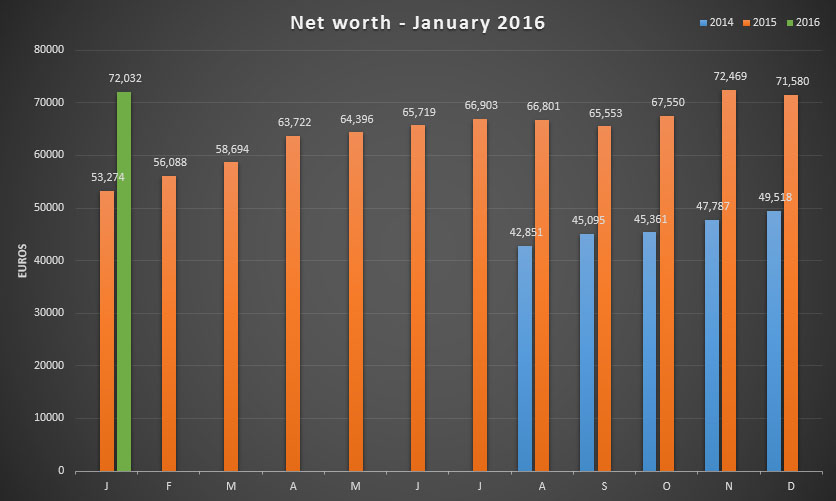

Compared to December, my net worth grew by a measly €452 even though I managed to save over €4,000 in the same time frame – ouch. Losing money is never fun, but January shows once more that the only thing I control with regards to financial independence and early retirement is my habit of consistently saving and investing any excess cash.

Even though I managed to save almost €24,000 in 2015, the overall asset growth of my portfolio doesn’t show a similar jump. The 0.63% increase of December and 1.23% loss in November clearly are the culprit here. However, with most stock markets being down almost 10%, things could have been a lot worse.

Two elements kept my portfolio from plunging by that much. First, the dividend stocks I own appear to be less volatile than most market indices. While the S&P500 is down 8% and the Euro Stoxx 50 lost over 10% YTD, my dividend stocks only recorded a 6% loss. The ETF portion of my portfolio nevertheless saw a similar decline as the Euro Stoxx 50.

Second, I keep a relatively large percentage of my portfolio in cash. I prefer the safety of cash savings as a cushion should I fall on hard times – nothing beats sleeping like a baby, after all. On top of that, cash allows me to take advantage of certain opportunities, both in and out of the market

You can find a detailed description of my dividend growth stocks, exchange-traded funds and cash below. I also highlight their performance since the time of purchase. Foreign securities were converted to Euros using the last-known exchange rate.

Dividend growth stocks

Returning visitors know that dividend growth stocks make up the bulk of my portfolio because I enjoy building a stable and passive stream of income. At the moment I’m using all dividends to fuel the compounding effect of my investments and I’ll continue to do so until I decide to retire early and live off of them.

That’s why December’s massive dividend income was used to increase my positions in American telco AT&T (NYSE:T) and Anglo-Dutch consumer goods giant Unilever (AMS:UNA or LON:ULVR). As a matter of fact, last month’s dividends bought me almost six additional shares of AT&T, thus boosting my forward income by another €6 after taxes – compounding at its finest!

I’m glad to be able to initiate a second purchase in AT&T, which is one of the first individual stocks I purchased way back in August 2014. I still believe the telecommunications provider is poised to do extremely well over the long-run even though organic growth in the US is likely to remain low. AT&T’s commitment to reducing its debt burden after the DirecTV acquisition combined with its juicy yield is what pulled me once more.

Similarly, the fact that I’m able to buy into a great business like Unilever again brings me great joy. Even now the dual-listed British-Dutch consumer goods manufacturer remains on top of my watchlist because of its pricing power in the developed world and its exposure to emerging markets. Of course, Unilever’s impressive dividend history doesn’t hurt either.

You can find the gains in absolute and relative numbers for each company in the table below. The cost basis for each position includes the price of the shares, a 0.27% stock market tax and brokerage fees.

| Ticker | Company | Shares | Cost basis | Mkt. value | Gain |

|---|---|---|---|---|---|

| ABI | AB Inbev | 22 | 2,385.18 | 2,343.00 | -1.77% |

| AFL | Aflac Inc. | 9 | 419.41 | 466.89 | +11.32% |

| T | AT&T | 80 | 2,352.46 | 2,492.55 | +5.96% |

| BLT | BHP Billiton plc | 110 | 1,908.56 | 883.80 | -53.69% |

| BP | BP plc | 92 | 507.24 | 412.18 | -18.74% |

| CAT | Caterpillar Inc. | 25 | 1,465.40 | 1,371.59 | -6.40% |

| DE | Deere & Company | 7 | 452.61 | 482.99 | +6.32% |

| DGE | Diageo plc | 75 | 1885.55 | 1,1,754.87 | -6.93% |

| ENG | Enagas SA | 50 | 1,258.60 | 1,258.50 | -0.01% |

| GE | General Electric | 22 | 450.70 | 574.37 | +27.44% |

| GSK | GlaxoSmithKline | 33 | 610.15 | 586.17 | -3.93% |

| HOME | Home Invest Belgium | 30 | 2,682.00 | 2,754.30 | +2.70% |

| INDV | Indivior plc | 10 | 3.89 | 21.77 | +459.52% |

| IBM | IBM Corp. | 6 | 736.76 | 714.78 | -2.98% |

| JNJ | Johnson & Johnson | 20 | 1,769.41 | 1,777.78 | +0.47% |

| KIN | Kinepolis Group | 40 | 1,399.25 | 1,536.00 | +9.77% |

| MCD | McDonald's Corp | 14 | 1,003.47 | 1,477.17 | +47.21% |

| MUV2 | Munich RE | 14 | 2,582.65 | 2,426.20 | -6.06% |

| NG | National Grid plc | 100 | 1,332.11 | 1,220.46 | -8.38% |

| NOVN | Novartis AG | 12 | 1,061.53 | 882.12 | -16.90% |

| PG | Procter & Gamble | 23 | 1,594.66 | 1,580.12 | -0.91% |

| QCOM | Qualcomm Inc. | 9 | 520.23 | 377.90 | -27.36% |

| RB | Reckitt Benckiser plc | 10 | 630.34 | 783.96 | +24.37% |

| ROG | Roche Holding AG | 5 | 1,233.71 | 1,173.32 | -4.89% |

| RDSB | Royal Dutch Shell | 110 | 2,956.64 | 1,960.20 | -33.70% |

| S32 | South 32 Ltd. | 48 | 20.04 | 27.62 | +37.81% |

| KO | The Coca Cola Company | 17 | 540.05 | 646.51 | +19.71% |

| FP | Total SA | 45 | 2,045.95 | 1,694.25 | -17.19% |

| ULVR | Unilever plc | 90 | 3,170.00 | 3,276.37 | +3.36% |

| VZ | Verizon Communications Inc. | 20 | 785.07 | 814.11 | +3.70% |

| VOD | Vodafone plc | 188 | 536.19 | 531.13 | -0.94% |

| Total | 40,299.79 | 38,288.96 | -4.99% |

Exchange-traded funds

Usually I talk about how the exchange-traded funds or ETFs I own are way less exciting than the dividend growth portfolio detailed above, but that’s not actually the case this month. True enough, the set-it-and-forget it approach remains the same, but this month my ETFs lost over 10% on average on top of last month’s 7% loss.

From this information you could argue that dividend growth investing is a better investment strategy, but that would be false logic. I’ve noticed that the accumulating ETFs I own are simply more volatile, both when the market goes up and when it seeks a new floor. Besides, dividend growth and index investing pursue completely different goals.

I added another 7 shares to the iShares Core MSCI World ETF to rebalance the regional diversification of my funds.

| Ticker | ETF | Cost basis | Mkt. value | Gain |

|---|---|---|---|---|

| IWDA | iShares Core MSCI World | 5,697.59 | 6,192.01 | +8.68% |

| IEMA | iShares MSCI Emerging Markets | 1,214.59 | 1,035.72 | -14.73% |

| IMAE | iShares MSCI Europe | 3,561.94 | 3,483.04 | -2.22% |

| Total | 10,474.12 | 10,710.77 | +2.26% |

Other

A large part of my portfolio still consists of cash-based savings, as explained in the first couple of paragraphs in this article. Obviously, the numbers here don’t change much, apart from a little bit of interest and monthly contributions into my personal tax-advantaged pension fund. On top of that I am still rebuilding my emergency fund, which results in a €1,000 jump compared to December.

| Name | Cost basis | Current value | Gain |

|---|---|---|---|

| Pension fund | 1,860.00 | 2,010.92 | +8.11% and 30% tax break |

| Savings account | N/A | 18,000.00 | N/A |

| Emergency fund | N/A | 3,021.55 | N/A |

| Total | 23,032.47 |

Going forward

To conclude, I sinned against Warren Buffett’s number one rule: don’t ever lose money – whoops! However, it’s unlikely that the current dent in my net worth will have any meaningful impact on my journey towards financial independence, especially over the long-run. In addition, for as long as the stock market trades a little lower I’ll take advantage of the higher dividend yield most companies offer.

The most important take away here is that the money you save up starts to live a life of its own. One month it’ll compound daily and earn you huge gains, while another month it’ll sink lower because of all sorts of external factors. Over time, however, your hard-earned savings will steadily multiply, albeit with the odd stumble along the way.

Thank you once again for reading and for your support – I appreciate it immensely.

Lovely update NMW, well actually maybe we should say “lovely considering what’s going on around us” update… 🙂

Having said that, these are the periods where a Dividend investor comes out, it’s hard to keep ones’s cool when markets are down and there are signs of “2008 redux” at the horizon… But as you wrote, in the end, provided that the stocks that we selected don’t do anything “strange”, a dividend investor looks at other factors, so has an easier life during a stormy patch.

I am out buying shares right now, did you do any trades this month?

Again compliments for the job so far!

Ciao ciao

Stal

Sweet post. Nice additions to the portfolio as well. If I had a 100k to invest in shares right now, they would definitely be between them. With the oil price going mostly down, maybe it’s a good moment to buy some additional Shell’s too? I will be adding some more when my paycheck comes in.

Gr

Nice update. I would guess that there are not many portfolios that have not seen at least some serious decreases in value these last weeks. I mostly see it as an opportunity to buy. And with a dividend growth strategy you should have a long term focus anyway.

Keep in mind you haven’t realized any losses. So you haven’t really lost any money, yet. If you sell all your stock now like many investors are, you will lose a bunch of money. Since we mostly buy and hold, hopefully our stocks turn around later in 2016.

Its impressive you still managed to generate an increase in overall net worth! We would like to see you do that again once your portfolio grows over 6 figures 😉

Without joking, seems that you could use some of your cash savings and average down on some of the oil and mining stocks (and/or ETF’s). Considering your very healthy savings rate, you would replenish the cash pile in no-time anyways. We doubt you would sleep any worse…..

Even though I’m an etf guy, I like your portfolio. Lots of consumer staples and oil stocks. Saw a presentation for 2016 yesterday. It should be the time for oil stocks. I wish I had your finantial view at your age. Ok that didn’t sound like I’m 32 😉

It’s a shame I didn’t go all in at the time of this previous post. Experts were convinced markets were at a turning point.

Hi NMW,

Looks like a pretty good month to me and you were still able to increase net worth overall.

What’s the % allocation between your ETFs that you’re aiming for – is it 60/10/30%?

Best wishes,

-DL

Congrats on increasing your net worth! When do you expect to reach your first $100,000?

Hi NMW! Long time no post! Hope you keep up the good work on this blog – I find it very valuable and motivating!

I second Bram’s remark; looking forward to new posts.

Miss your updates. Dividend income, buys, etc. When can we see a new post?

Looking forward to see your 2016 targets, learn about your real estate acquisition, your bike rides,…

I hope all is well NMW! It’s been awhile dude, and you are by far my favourite blogger!

Pat.

I got a feeling the stock market kicked you recently in the nuts. Trust me I know the feeling. I put a lot of time and effort in moving forward the frugal way and then you see your investments melt away like snow in the sun. So I’d run for the exit on the worst time possible. I learned that an aggressive portfolio isn’t 4 me, the hard way.

So prove me wrong and don’t tell me your eating fucking waffles now 😉

Yep year over year div increases are the goal. It is never a loss until you sell.

Cheers,

DFG

Its kind of stupid to say its a loss only when you sell. You sell when you believe there is a permanent impairment of one of your holdings. Some stocks go down for good reason. Dividend increases only kick the can down the road. See BBL or KMI!

Hi NMW, were you able to retire already? 😉

I miss your updates too, hope all is well 🙂

How´s it going over there in Belgium. I guess the last two weeks have provided some relieve to portfolios! looking forward to hear some news!

I guess NMW has cancelled his internet subscription in order to improve his savings rate 😉

You are doing a great job and the fact that you started your journey to financial independence at such a young age is inspiring. well done 🙂