Inflation has shot up to the highest level since 1982 in Belgium and stood at a whopping 8.31% in March. On every 100 Euro we owned last year, we’ve lost over 8 Euros worth of purchasing power. Of course, Belgium is not alone, with many other countries’ citizens experiencing a much higher cost of living compared to just a few months ago. Should we be worried? And what can we do to protect our wealth and financial independence?

To many of us it feels like the economy is on fire, using our piles of hard earned money as firewood. With the Federal Reserve and the European Central Bank having cranked up quantitative easing to the max during the COVID pandemic, and now the Russian Federation invading Ukraine, it’s no surprise the international monetary system adjusts to loads of fresh money in the market and to exploding energy prices.

In March energy experienced an inflation rate of 57.22%, making up 4.82% of the 8.31% total inflation rate. Core inflation therefore stood at 3.75%, also much higher than the ECB target of 2-3% on average. The “inflation is transitory in nature” mantra of the Fed and ECB has long ceased to be believeable now that second-round effects drive up core inflation more and more.

Second-round effects?

Exactly. While higher energy prices are immediately felt at, for example, the gas pump, our long-term expectations of inflation put additional upward pressure on inflation. On top of that, many companies protect their bottom line by increasing prices to offset their elevated energy bill, thus triggering more inflation.

In a worst case scenario, second-round effects could turn into third-round effects, into fourth-round effects, into… You get the picture. My German readers know all too well the devastating effect inflation can have when it spirals out of control and turns into hyperinflation.

Inflation is transitory, right?

As mentioned above, the Federal Reserve and European Central Bank have long upheld the image that inflation was going to be transitory because it was the result of the end of the COVID pandemic. With the continuing high inflation worldwide and its slowing effect on global economic growth, that line of thought sounds less and less plausible each day.

Ultimately, when taking a long-enough timeframe everything becomes transitory. But that doesn’t help us in the here and now. We are losing 8% of our savings now, not in the future.

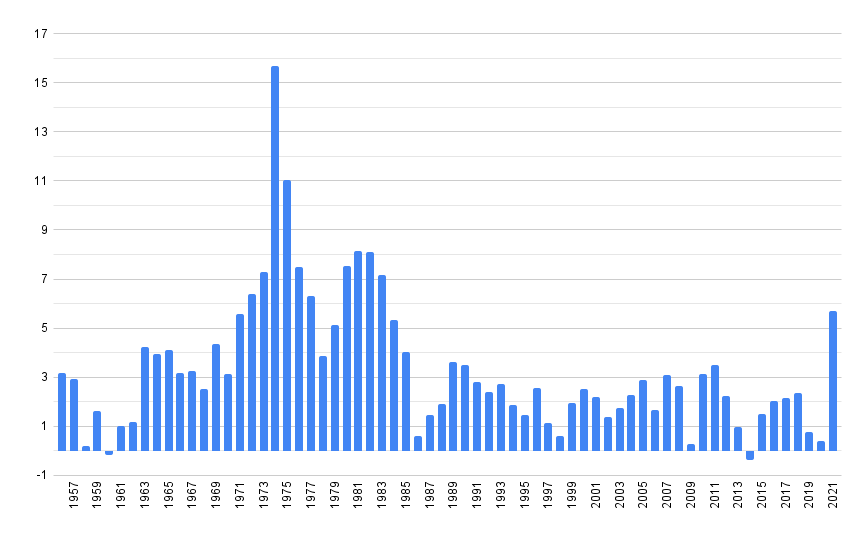

We should, however, ask ourselves: is it important that inflation is transitory? Let’s take a look at the levels of inflation in Belgium in the past 65 years.

On average we have managed an inflation rate of 3.3%, taking into account extreme peaks in the 1970s with nearly 16% inflation at one point, and lows of -0.38% in 2014.

As you can see, inflation has always been a core component of modern economic theory. When compounding interest is the yin of the economy, inflation is its yang. Therefore most central banks strive for an optimal level of inflation of around 2-3% on average. And that’s the number you should be taking into consideration when thinking about protecting your wealth.

Therefore it’s not important whether inflation is transitory or not. Inflation is always an element you should be mindful of, especially when you are deciding on assets that should sustain your financial independence. Simply put, and in an ideal scenario, your money should always yield a higher return than the rate of inflation.

Your personal inflation rate and expenses

But wait, maybe you are not the average consumer? The total inflation rate of a country is the average price movement of a basket of weighted goods and services that most people use. Since averages obscure individual data points, it’s therefore completely possible that your personal inflation rate is much higher or lower than the country’s level of inflation.

Let’s say, for example, that you don’t own a car and your home has the perfect energy density so that you your hardly consume any energy compared to most other people. In Belgium, your personal inflation rate could therefore be much closer to the core level of inflation (3.75%) than the total inflation (8.31%) in March.

3.75% is a whole lot less daunting and more manageable than 8.31%, right?

Be sure to check out how your country calculates its inflation numbers, so you know which goods and services are the biggest contributors to the actual inflation. Maybe the increased price pressure doesn’t hurt you as much, and even if it does, you could potentially adapt your spending a bit to reduce the effect on your savings.

Protecting your income

While it is possible to reduce your exposure to high inflationary goods and services, it would be a pipe dream to have inflation-free expenses. As such, it’s equally important to protect your income and make sure it grows with inflation.

If you’re not financially indendent yet, it’s highly likely that the majority of your income stems from wage labour. At an 8% inflation rate most of us are effectively working a full month for free this year compared to last 2021. That is unless your employer (automatically) adjusts your paycheck to inflation. Even though it’s a rare thing in the majority of countries, Belgians usually enjoy an automatic wage indexing mechanism.

(Hello, faster second-round effects!)

When your employer doesn’t automatically adjust your paycheck to inflation, be sure to ask for an appropriate raise the next time that topic comes up. Or if you’re feeling particularly confident in your job prospects you can go ask one right away. Remember: you’re working a full month for free compared to last year if you don’t get at least an 8% raise.

For those of us enjoying a wealthy and lavish financially free lifestyle, there’s sadly no boss you can turn to and ask for an appropriate raise. As mentioned above, you’ll have to make sure that your assets yield a higher return than the rate of inflation. A tough position to be in considering that a lot of asset classes don’t perform well under inflation and certainly not to the tunes of 8% on a yearly basis. More on this later.

What to do with your savings

Losing 8 Euros for every 100 Euros saved isn’t a great deal, so you might think it’s no use to save anything at all and throw your good savings practices and rate out of the window. You’d be 100% correct if you’d put your money in a low-yielding savings account.

However, a far superior strategy is to remain invested in either cashflow positive assets like real estate or the stock market.

Real estate, together with gold and other commodities, is often seen as the ultimate hedge against inflation. People need somewhere to live, so land and property values often keep track of rising inflation. As a result, landlords are able to steadily increase the amount of rent charged, which often keeps pace with inflation.

Another option is to remain invested in the stock market. It doesn’t take a genius to figure out that companies will do anything to keep their margins, earnings and bottom line in tact. They’ll therefore try to increase their prices to offset the effects of inflation on their earnings potential. Some companies have greater pricing power, mostly because they provide essential goods and services, while some do less. Overall, however, a well-diversified group of businesses should help you weather any inflation ahead.

This, too, shall pass

Wait, No More Waffles, didn’t you earlier mention that it didn’t matter whether inflation was transitory or not?

Absolutely, in the long-term it hardly matters for your investments and assets whether inflation is currently at 8%. You can, on average, expect most asset classes to provide a yield far above the 2-3% inflation rate. The (in)famous Trinity study that formed the basis for the 4% rule many early retired people base their necessary savings and withdrawal rate on even took into account the effects of inflation.

Furthermore, if we take a look at the inflation chart above, you should always remember “this, too, shall pass”. Our current situation is unique in certain aspects, but not in all. Inflation goes up, it goes down, but the world keeps chugging along. People keep buying life’s necessities, continue going to work, and even keep finding entertainment to enjoy – surprise!

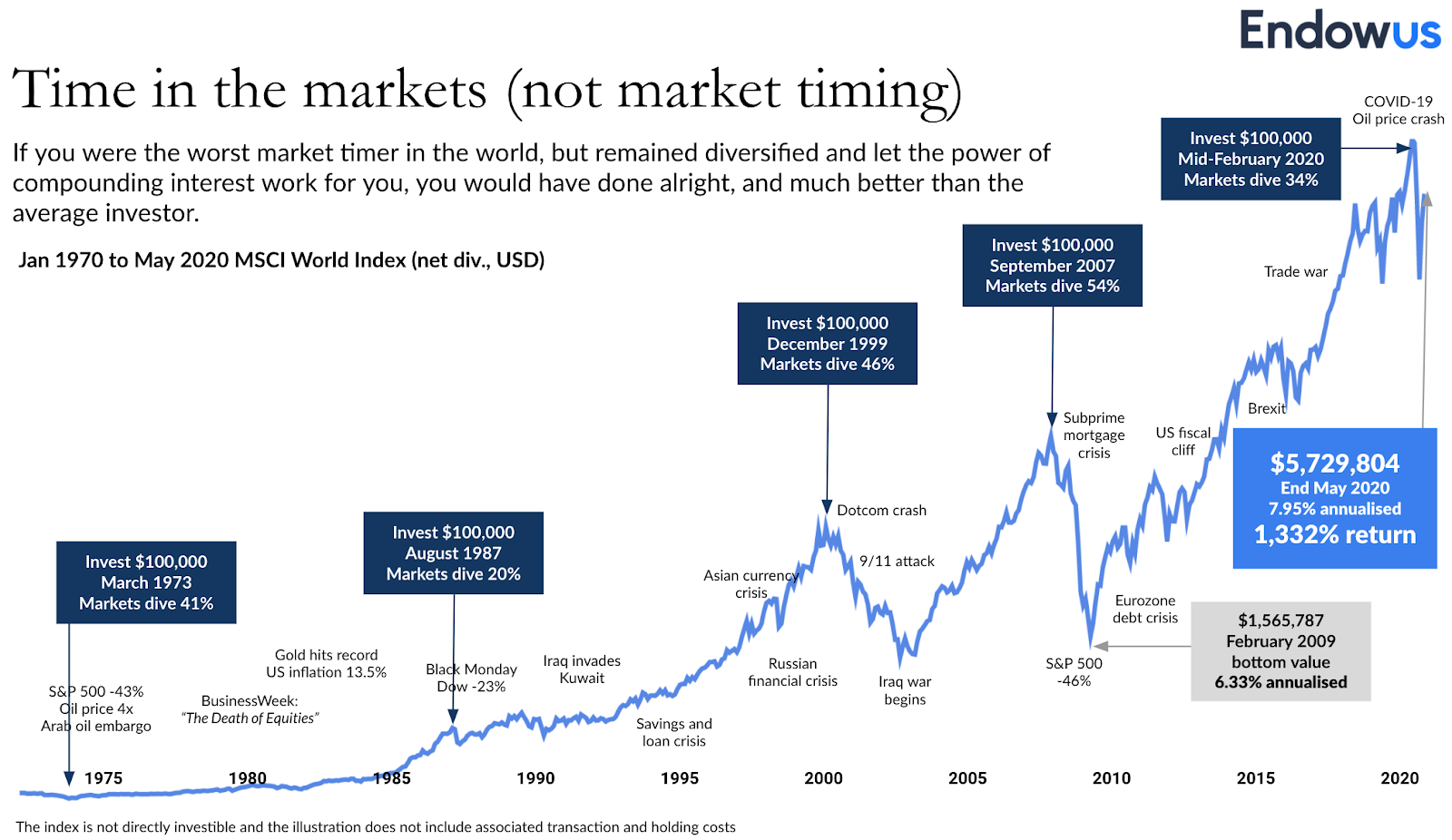

If you’re trying to become financially independent, or already are, the most important thing is to keep saving as much as possible and remain invested as much as possible. Time in the market is infinitely more valuable than timing the market.

Let this infographic sink in:

Even if you’d bought the MSCI World Index, like I do with my ETF strategy, at the five largest price peaks since 1970, you have an average annualised rate of return of 7.95%. That’s almost 5% more than Belgium’s average level of inflation during the same time frame.

So, take a deep breath, ignore the noise, and let your investments do the heavy lifting. Financial independence requires a long-term view.

How do you feel about inflation? Do you deploy specific strategies to deal with it, if you worry about it at all?

Here’s five bonus ideas to deal with inflation:

- Take on additional debt with a low enough interest rate. For example, my mortgage interest rate is 1.27% for the next 25 years, giving me an immediate return of 7% at current inflation levels.

- Become more self-reliable! Add solar panels to your roof, install a rain water collection system, grow your own vegetables, and use your bike more to get around.

- Start a luxury handbag business.

I just found out you were back, and notice you’re already gone again! 🙂

Good luck and see you back on the next update.

Hello NMW, Like you I stay invested in the markets. And while financially sub-optimal, I do feel less stress using my cash buffer in retirement so I don’t have to withdraw from my investments and allow them to recuperate somewhat.